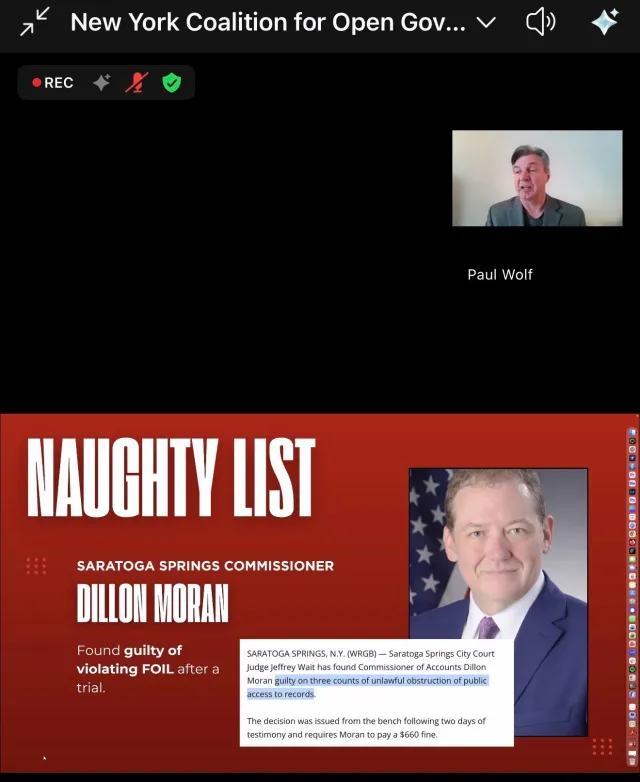

Mike Brandi and Dillon Moran Honored and Dishonored by NYCOG

The New York Coalition for Open Government, a highly respected not-for-profit group that advocates for better transparency in government, has issued awards at its annual meeting. In the case of Saratoga Springs, we received two awards. Both were well deserved.

These awards would, under normal circumstances, be an enormous embarrassment to the Saratoga Springs Democratic Committee, which has uncritically promoted Moran and has been disturbingly silent about the events that prompted the awards. It is yet another confirmation of how oblivious the Committee is to the profound importance of the New York State Open Meetings Law and the best traditions of democracy.

Press Release

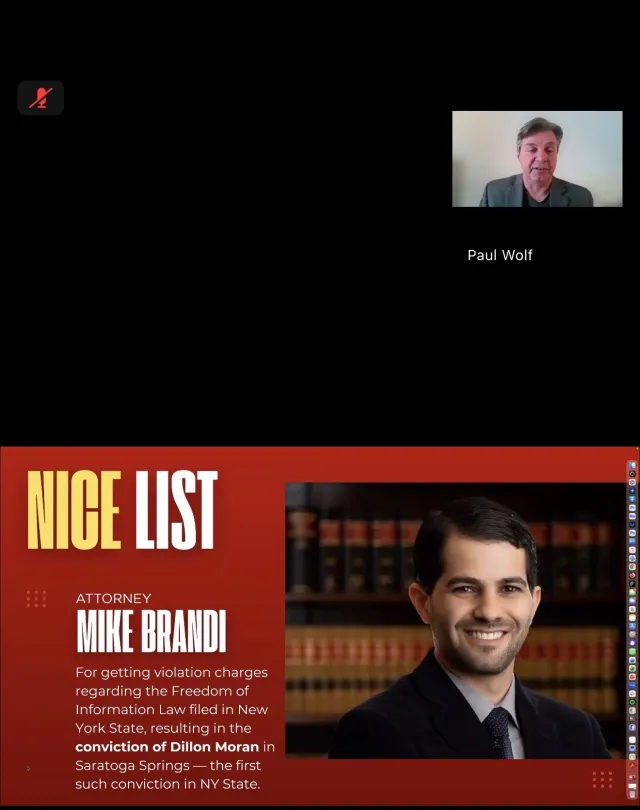

Mike Brandi Honored on New York Coalition for Open Government’s Annual “Nice List” for Leadership in Government Transparency

Saratoga Springs, NY — Mike Brandi has been honored with inclusion on the New York Coalition for Open Government’s annual “Nice List,” recognizing individuals and organizations who have demonstrated a strong commitment to transparency and open government across New York State.

The New York Coalition for Open Government is a non-profit, non-partisan organization dedicated to promoting open, honest, and accountable government at all levels throughout New York State. At a press conference held today, the Coalition announced its annual “Naughty and Nice List,” which highlights individuals who have either advanced—or undermined—the principles of open government over the past year.

Brandi was recognized for his role in exposing and pursuing unlawful conduct that obstructed public access to government records. His actions were central to bringing to light the conduct of outgoing Saratoga Springs Commissioner of Accounts Dillon Moran, who issued multiple false certifications in an effort to conceal public records maintained on his personal email account and social media.

In a landmark case, the Saratoga Springs City Court found Moran guilty after trial on three counts of unlawful obstruction of public access to records. As a result of that conduct, Moran was one of ten individuals statewide named to the New York Coalition for Open Government’s “Naughty List” for acting against the public’s right to know and unlawfully obstructing transparency.

“Open government laws only matter if they are enforced,” Brandi said. “This recognition underscores the importance of holding public officials accountable when they attempt to hide public records or evade transparency requirements.”

Sanghvi and Moran End Their Tenure On The Council With Just More Disinformation

Saratoga Springs is finally coming to the end of the ordeal of having to listen to disinformation from Finance Commissioner Minita Sanghvi and Accounts Commissioner Dillon Moran. Still, even for them, the chaos and dishonesty they have engaged in discussing the mess Sanghvi created with the 2026 budget takes a lot of nerve.

In the November 20, 2025, edition of the Saratogian, its readers were subjected to the magical thinking of Sanghvi and Moran, in which events are twisted beyond recognition.

Sanghvi’s Twisted Self-Congratulations

According to the city’s charter, the Finance Commissioner is supposed to spend months working with each department’s executive staff to craft the next year’s budget. The budget is supposed to reflect the Commissioner’s best thinking on balancing the city’s resources with its anticipated income.

In October, with less than two months until the budget’s required adoption date, Sanghvi suddenly announced that the city was in a deep financial hole. Her response was classic partisan abuse. To close this hole, Sanghvi’s (a Democrat) proposed budget eliminated funding for the Mayor’s (a Republican running for office) department for non-profits, most of which were devoted to homelessness, as well as other key services like school crossing guards.

This is what Sanghvi told the Saratogian on October 9, 2025,

“I could not take money from our police or public works department and then give that money to nonprofits. This is not an easy decision. This is not something we did lightly, but we had no other way of doing this.”

In this same article, she dismissed the idea of raising the property tax rate to address the shortfall:

Another option Sanghvi pointed out, though she added that she did not (sic) believe “city residents should not be facing the burden of rising property taxes every year” and that “2% is more than enough.”(Emphasis added)

Saratogian Newspaper

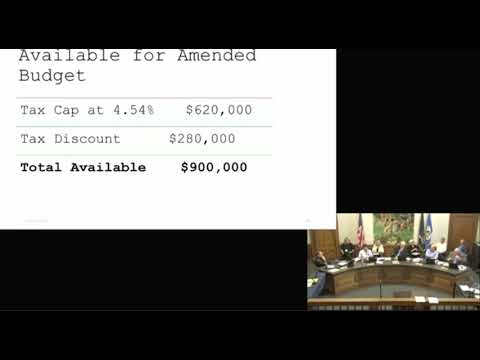

Sanghvi doesn’t explain where the money will come from to put the $900,000.00 back in the budget. Magic!

According to the November 25, 2025 Times Union, Sanghvi transferred $1,810,000.00 from the city’s fund balance (reserves) and $500,000.00 from the city’s retirement reserve. So we will run a deficit of at least $2,310,000.00 next year. I have no idea whether it is prudent to take $500,000.00 away from the city’s retirement reserve. It is troubling that Sanghvi supposedly overestimated by $500,000.00 what would be needed next year to meet our obligation regarding the retirement system.

Sanghvi’s Magical Thinking

As it turned out, the final budget was very different from her original proposal. In addition to raiding the city’s reserves and its retirement funding, Sanghvi reversed her position on raising taxes. Her new budget will now benefit by raising taxes by 4.53%. This, of course, comes after the election, during which she was campaigning for a Count Supervisor position.

It is important to note that based on Sanghvi’s budget, the city ran a deficit of $3,500,000.00 during the current (2025) year. It is rather stunning that Sanghvi only revealed this fiscal hole after her successful campaign for County Supervisor.

I’m sorry that, for many, the Saratogian articles are behind a paywall, as it is impossible to summarize the rambling, contradictory remarks Sanghvi made to the Saratogian in defense of what she did. Sanghvi effusively congratulated herself and her work with the community for reinstating her own cuts.

Take this statement from Sanghvi:

They [JK: The community?] said very clearly that they wanted to fund the RISE shelter, the homeless, Franklin Community Center and all these other organizations, which are doing incredible work in our community and that they were fine with the 4.5% tax increase. I think it was important for the public to come to that conclusion themselves and say, ‘yes, we want this tax increase to pay for this. And I think that’s sort of the goal that we achieved here.”

This may be the way Sanghvi wants this debacle remembered, but it is not what actually happened.

In fact, Sanghvi faced significant pushback from Mayor Safford, Public Works Commissioner Chuck Marshall, and Commissioner Coll on her budget from the start.

This is Coll’s recollection:

As soon as I saw the Comprehensive Budget unilaterally presented by Commissioner Sanghvi, I knew we were in trouble. The proposal included no funding for school crossing guards, contractual obligations, or our vital nonprofits such as the homeless shelter and the Senior Center. I strongly advocated for a tax increase to our legal limit (4.5%) and for using fund balance to support our nonprofits. Fortunately, Mayor Safford, Commissioner Marshall, and I reached a consensus to address the needs of our most vulnerable residents, as Commissioner Moran was absent from this particular budget workshop. The video of this meeting, dated 11/14/2025, will corroborate and set forth the truth of this matter, including that Commissioner Sanghvi’s budget did not provide funding for these nonprofits from the outset.

Commissioner Tim Coll

Dillon Moran’s Memory Hole

Moran was the sole vote against adopting the budget. He attributed his vote to the budget’s failure to include funds to address the city’s alleged water issues, issues he claimed he raised when he ran for DPW Commissioner seven years ago.

According to the Saratogian article, Moran said:

“The budget does nothing to put forward money to invest in the most important thing we provide to our citizens, which is clean, potable, consistent drinking water. I, in good conscience, cannot vote for that budget. The biggest issue facing this community. Period.”

Moran to the Saratogian

So if Moran was alarmed about the lack of money in the budget regarding water, why didn’t he offer an amendment to address his allegation?

Instead, he offered the following shrill warning to the Saratogian:

“The budget does not include money to address the issues in any sort of meaningful way. We are facing a $40 million investment that I called for seven years ago, when it was $24 million and it’s $40 now. If we don’t do something about it today, it’s going to be 50 (million), and then 60 (million), and then we’re going to have a major failure and then big sections of our community could be without drinking water.

“And if they’re without drinking water for a certain period of time, and those pipes sit dry, that’s it.”

Dillon Moran

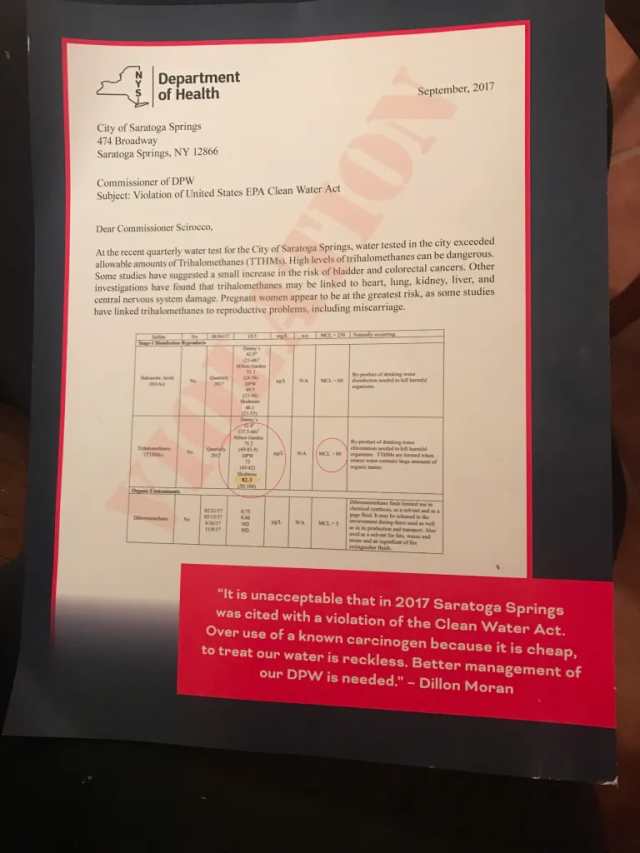

Apparently, Moran does not remember that his campaign for Commissioner of Public Works at the time was deep-sixed when it was revealed that a campaign mailer he had sent included a forged letter purportedly from the New York State Department of Health supporting his wildly false accusations about the state of the city’s water supply.

Here is a post documenting Moran’s folly in which he falsified the NYSHD letter.

This is the mailer containing the forged letter from the New York State Department of Health that Moran sent out in his attack on the late Public Works Commissioner Skip Scirocco.

Minita Sanghvi’s 2026 Budget-More Chaos

This blog has documented the numerous missteps in handling the city’s finances by Minita Sanghvi since she became the Saratoga Springs Commissioner of Finance.

Under the city charter, Sanghvi is responsible for preparing the city’s budget each year, which must be adopted by November 30. As this deadline approaches, Sanghvi’s years of mismanaging the city’s finances have finally brought the city to the verge of a financial crisis. How severe a crisis it is, even now, is hard to determine, though, as the financial indicators Sanghvi should be providing are missing.

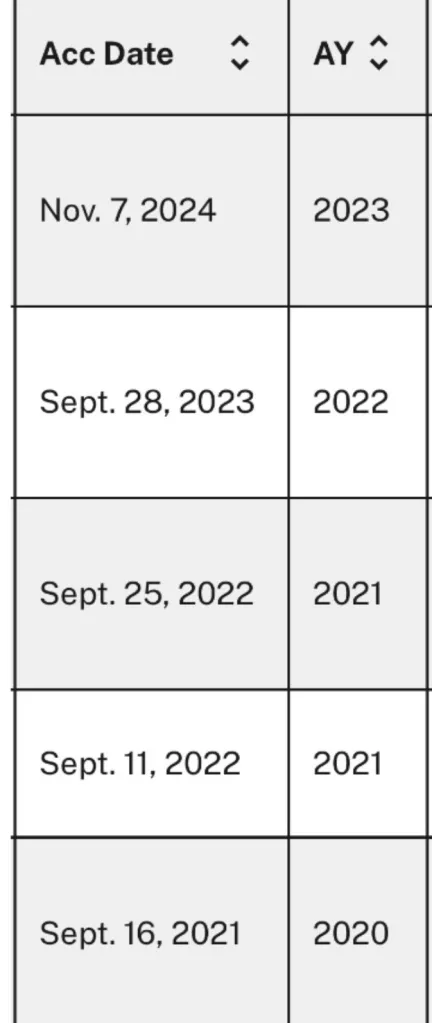

One of the key documents that should have been an important tool for the Commissioner to use in understanding the city’s financial condition and planning for the 2026 budget was due September 30. As of the time of this blog’s posting, the audit has finally been placed on the agenda for the November 18, 2025, meeting; however, the link to the actual audit included in the agenda does not work.

The tardiness of this audit is not new for Sanghvi. The 2023 audit also missed the September 30, 2024, deadline and was not submitted until November 7. This was coincidentally only days after the November 2024 election in which Sanghvi was running for the State Senate. As the audit included damaging items regarding her handling of the city’s finances, it is no small wonder that she delayed releasing it beyond the required date and after the election.

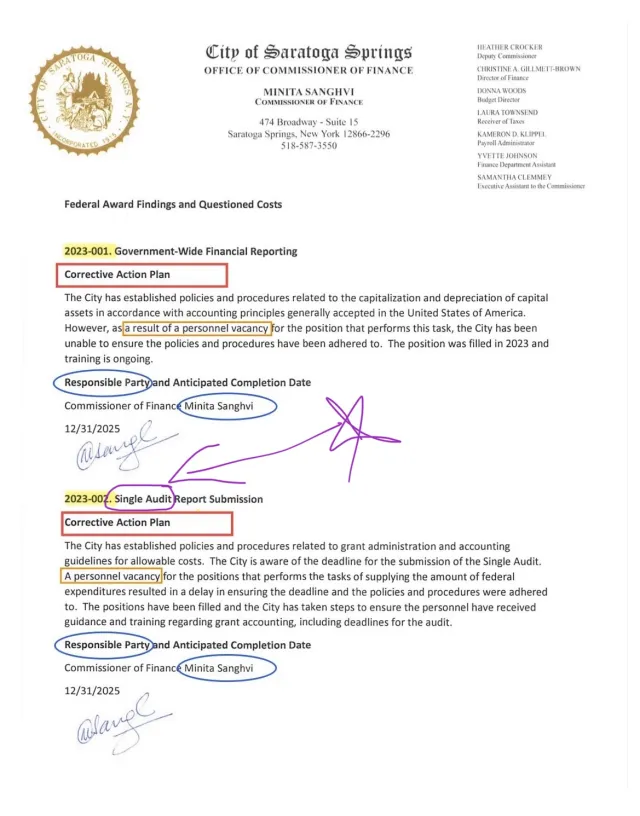

In addition to tardiness, Sanghvi is criticized in the audit for failing to follow “accounting practices generally accepted in the United States.” She blamed this problem on “a personnel vacancy.”

In her response to the audit (below), Sanghvi admits that she had failed to meet the “…deadline for the submission of the Single Audit.”

You would think that, having been criticized in the 2023 audit for being late, she would be particularly diligent about ensuring the timeliness of the 2024 audit release. You would be wrong. She is late for the second consecutive year.

I am unaware of any previous Finance Commissioner failing to submit the audit on time, let alone failing to do so twice.

I contacted Commissioner Sanghvi, asking why, yet again, the audit is so late this year. In a phone conversation, she blamed the problem on the alleged failure of the Mayor’s office and the Department of Public Works.

I contacted Deputy Mayor JoAnne Kiernan and DPW Commissioner Chuck Marshall regarding Sanghvi’s allegation. Both officials told me that Sanghvi had not contacted them about any missing information.

I then sent the following email to Sanghvi, requesting any documentation that she or her staff had provided to the executive staff in either the Mayor’s office or the DPW regarding the urgent need for missing information.

The Email

| John Kaufmann < | Tue, Nov 11, 7:00 PM (3 days ago) | ||

| to Minita, Tim, Dillon, John, Charles.Marshall | |||

Minita:

Thank you for returning my call. As you are aware, we discussed the city’s lack of an audit. BST, our auditor, was required to provide the city with its audit by September 30. In turn, your office was required to submit the audit to the city council and the public by November 1.

You blamed the failure to meet the city’s deadlines on the mayor’s office and the Department of Public Works.

On September 25, you emailed DPW about missing information. They informed you that the information you were looking for had been uploaded to a folder shared by DPW and Finance on August 7. You had the information. If there was any confusion about the information, please let me know why you waited until September 25, five days before the audit was supposed to be completed, to contact DPW?

Regarding the mayor’s office, you never contacted the mayor or his deputy about this issue. Apparently, someone from your office has contacted the planning department regarding a matter involving grants. (In the previous audit, you were criticized for your failure to properly manage the fiscal elements of these grants.) Notably, your office did not raise the issue until mid-October. As the audit was required to be completed by September 30, can you explain why this was not addressed earlier? If this was pressing and not being done, why didn’t you email the mayor or his deputy? Please provide any documentation regarding the attempts made by your department to obtain this information.

Audits are at the heart of accountability and of transparency. What’s most alarming is that you do not seem particularly concerned about the failure of Finance to provide this audit, which should have been available before the election. Given the criticisms in the auditor’s 2023 report, one must wonder whether the 2024 audit will contain unflattering findings.

My key question to you is why you did not advise the council that you were unable to meet your obligation under the charter to provide them with this vital document?

Radio Silence

As usual, I received no response. I submit that there was no response because Sanghvi has no documentation. She is guilty of an inept attempt to cover up the failure in her office. I do not think it is unreasonable to consider that she has suppressed the latest 2024 audit report because it would reveal more problems in her office, particularly in a year when she was running for Supervisor.

Sanghvi’s October Surprise

As the Commissioner of Finance, Sanghvi is responsible for monitoring the city’s spending.

In May, the city agreed to fund RISE (the provider of a homeless shelter for the city) for approximately half a million dollars. Sanghvi not only voted for the resolution, but she waxed on about the value of their service for our city.

In October, Sanghvi presented a budget that cut not only the funding for RISE, but also for all the not-for-profits the city had been supporting for years, including the Senior Center. The reason? The city was suddenly facing a $3,500,000.00 deficit for the current fiscal year, which is not yet over.

How could she not have seen this coming?

By May, when she supported spending $500,000.00 on RISE, she should have been aware of the looming budget problems.

It is a testament to her mismanagement that, up until October, when she was finally required to prepare the budget for next year, she said nothing at the Council table about the financial threat facing the city.

It is worth noting that Sanghvi was warned last fall, during the preparation of the 2025 budget, that her fiscal assumptions were overly optimistic. At the time, Public Safety Commissioner Tim Coll urged her to raise the city tax rate to 2%, as allowed by state law. Although she had raised taxes her previous two years in office, in 2024, she was running for State Senate and refused.

As has become painfully obvious, her budget for 2025 badly underestimated expenses and overestimated income. This was not her first time doing this.

As this blog has documented over the last four years, Sanghvi is far more interested in drama at the Council table than in devoting the very demanding time required to fully understand the city’s finances.

Understanding Just How Bad Sanghvi’s Budgeting Is

Under our charter, the Finance Commissioner is responsible for preparing the city’s annual budget. This budget is intended to be the result of thorough analysis and consultations with other city departments. While it is expected to be revised once it is proposed to the Council, it is intended to be a serious document that the Finance Commissioner would want to be adopted as is. This is because, unless a majority of the Council overrules the Commissioner’s proposal, it is automatically the city’s budget for the following year.

Sanghvi’s desire to defund all the not-for-profits (RISE, the senior citizens’ center, Judge Vero’s outreach/homeless court, and even school crossing guards) was supposed to reflect her determination that while these organizations were valuable, other city needs would take precedence.

Coincidentally, in an election year, these major high-profile nonprofit organizations that were cut are funded by the Mayor’s office, and these cuts were often portrayed as coming from the Mayor, not Sanghvi.

According to reports, although the public has yet to see the changes, Sanghvi has reportedly now restored these cuts.

Sanghvi Blames Other Departments For The Failure Of Her Department and Gibberish and Confusion Over What The City’s Reserves Are

As of this Friday, November 14, Sanghvi was still not taking responsibility for the late audit and continued to demonstrate a fundamental ignorance of the city’s finances.

At the pre-agenda meeting on Friday morning, Sanghvi again blamed unnamed departments for the audit delay. She informed her colleagues that her office had met with the auditors in mid-October to discuss the remaining information they needed. As the audit was supposed to be completed by the end of September, she self-documents the tardiness of her own office in completing the audit.

In a budget hearing that same day, Sanghvi was asked to provide the Council with accurate information on the city’s fund balance. The “Unassigned Fund Balance” is the technical term for the city’s reserves. In addition to raising taxes, one way to address the city’s deficit is to tap into its reserve fund. It is obviously important to know the size of the reserve in order to determine how it may be used to address the city’s deficit.

In this clip, Commissioner Coll attempts to determine from Sanghvi how much the city has in reserve to address the proposed budget shortfalls.

The Finance Commissioner serves as the chief financial officer (CFO) of the city. It’s hard to believe, as documented in the following video, Sanghvi was unable to answer Commissioner Coll’s repeated requests regarding the city’s reserves to address the budget for next year. As her frustrated response indicated, she did not know, and this is particularly glaring because, given the repeated requests for this number, she should have had the figure readily available.

Further, note how she distances herself from her staff in the video clip. When trying to explain what the city’s reserves are, she notes that the numbers she is getting are from her staff referring to her deputy and budget director as “they” as her budget director is shaking her head. So these are not numbers that she has analyzed and that constitute her financial analysis. Apparently, she is unable to read these reports on her own and adopt them as her own.

Thank You, Brian Wager

After thirty years with the city’s Department of Public Works, Brian Wager retires next Saturday.

Those of you who use the transfer station to dispose of your garbage and recycling, have probably been assisted by Brian. Always patient and good-humored, Brian was always available to give a helping hand.

When you see Brian, thank him for his service and wish him well in his retirement.

BK Keramati Goes to the Dark Side

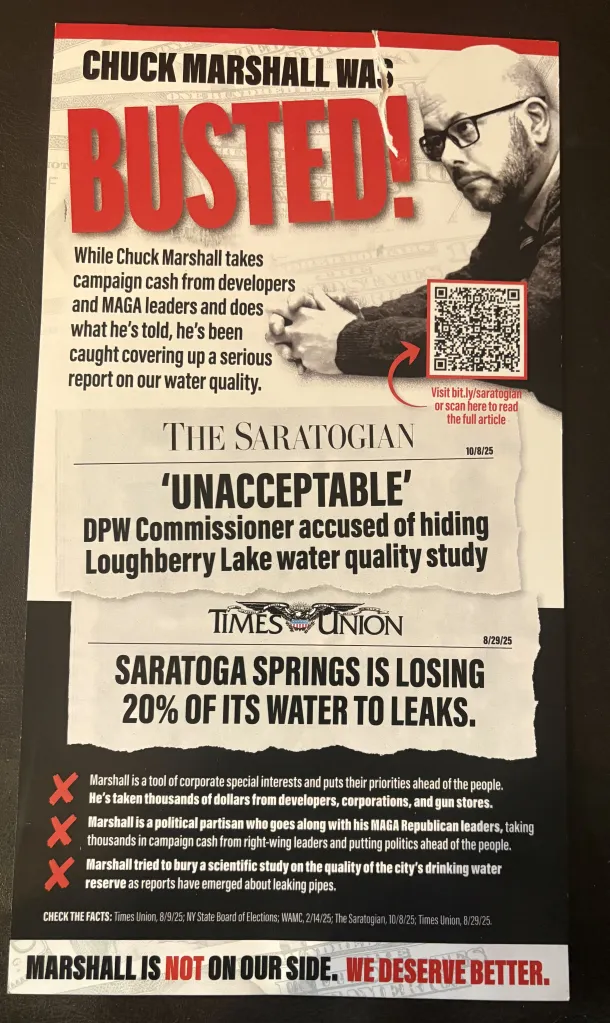

This is a mailer BK Keramati sent to Saratoga Springs voters.

Up until he began his campaign for Saratoga Springs Commissioner of Public Works, my encounters with BK Keramati over the years had always been pleasant.

While I supported his opponent, the current Commissioner, Chuck Marshall, I believed Mr. Keramati did not have the history of toxic behavior that other candidates endorsed by the local Democrats this year had. I assumed, therefore, that if elected, he could be counted on to interact civilly with his fellow Council members even if he did not always agree with them.

I was unprepared then for his toxic mailings and social media assaults on his opponent. His campaign became just another example of the ugly and vituperative behavior that the city has endured from the Democratic leadership over the last four years. What is sad is that, given Keramati’s reputation up until this point and his vigorous door-to-door campaign, he might well have won without stooping to this kind of dirty politics. Instead, he focused on false statements and assumptions to run a campaign that essentially was an attempt at the character assassination of his opponent.

The Water Report

One of Keramati’s main themes was to accuse Chuck Marshall of “hiding” a study of Loughberry Lake. Many of the issues with this aspect of Mr. Keramati’s disturbing campaign were explored in an earlier article.

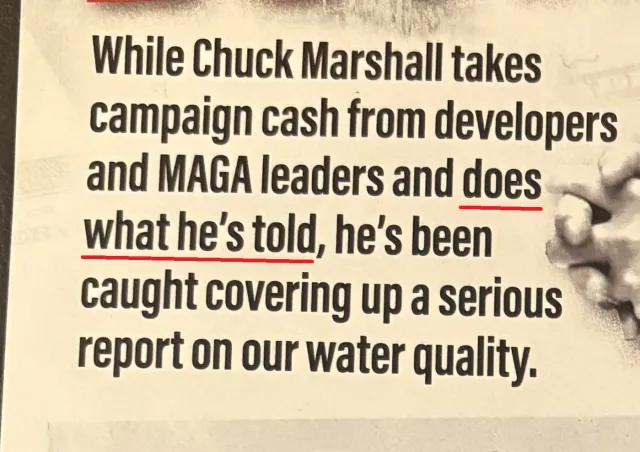

Suffice it to say that since Chuck Marshall immediately gave BK the report when asked and without making him FOIL for it (something that would have meant BK would have not gotten the report until after the election), it is difficult to understand how Mr. Keramati could, with any integrity, describe Marshall as being “caught covering up a serious report on our water quality” as he does in his mailer.

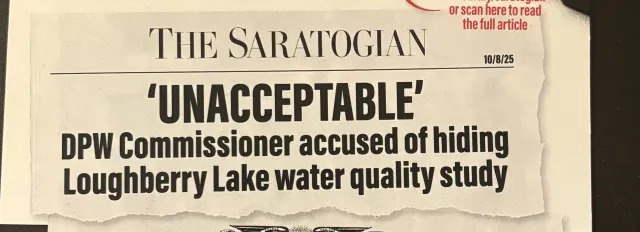

Fooling The Public

To provide credibility to his accusations, Keramati doctored an image of the Saratogian Newspaper (and others)in his mailers. This headline never existed. The tear at the bottom of the image was meant to convey authenticity.

An Assault On Marshall’s Integrity

Chuck received a considerable amount of money from, among others, individuals in the real estate industry.

BK could have legitimately pointed this out and raised questions about the extent to which they might influence Chuck’s tenure should he have won.

Instead, BK’s mailers went over the top, asserting that “he (Chuck) does what he is told” and he is “a tool of corporate interests and puts their priorities ahead of the people.”

Keramati provides no examples of Chuck having used his position to aid donors.

To the contrary, Chuck has had the opposite reputation as Planning Board Chair, where he was known for creating an environment of inclusion and respect, working with a board of diverse people, both politically and socially.

I recently spoke to Bill McTygue, who served on the Planning Board with Chuck. Bill had been on the Democratic Committee and probably supported Keramati, yet he was quite complimentary of Chuck’s leadership. I asked him specifically whether he observed any effort by Chuck to manipulate the board in favor of any developers. Bill said “no.” Bill observed that Chuck’s focus was on building a consensus among the board to make decisions.

So what does it say about Keramati’s character that he would tell voters that Marshal is a guy who “does what he’s told”?

Likewise, Keramati cites a donation Elise Stefanik made to Chuck’s campaign as evidence that “Chuck is a political partisan who goes along with his MAGA Republican leaders…putting politics ahead of the people.” Keramati again cites no evidence of this and appears uninterested in acknowledging that Chuck has publicly stated he did not vote for Donald Trump.

The Chuck Marshall I Wish People Had An Opportunity To Know.

Here is an anecdote that may help people to understand what kind of person Chuck Marshall is in comparison with the characterization of him put forward by Mr. Keramati.

When Chuck defeated Hank Kuczyinski, he inherited Michele Hill-Davis as his executive assistant, whom Kuczynski had hired. In addition to having been selected by his opponent, Ms. Hill-Davis is an active committee member of the city’s Democratic Committee.

I know for a fact that quite a few people told Chuck he needed to replace her. They argued that as his executive assistant, she would be privy to all the goings-on in his office. In effect, she would be a spy.

In classic Chuck style, he refused. He said he would not fire anyone without giving them a chance to demonstrate their ability to perform the work. Ms. Hill-Davis is still his executive assistant.

Unlike Keramati, Marshall’s campaign also reflected his character. It was positive without a breath of attack and recrimination.

Hope?

Keramati worked closely with Gordon Boyd, who energetically echoed and amplified Keramati’s campaign claims on his Facebook page, and Achim Bergmann, a professional political operative with national campaign experience and a member of the local Democratic committee. Both men BK chose to work with have a history of running toxic campaigns.

One can only hope that Keramati will show more civility and integrity at the Council table than he did in his campaign.

Why Can’t Dillon Moran Just Tell The Truth?

This blog has previously reported on the two years during which Saratoga Springs Accounts Commissioner Dillon Moran promised numerous dates for deploying the Short Term Rental (STR) portal, which property owners can use to register.

According to the timestamp on his campaign Facebook page tonight (November 3), on the eve of the election, Moran claims that he deployed the software last Friday (October 31) and that his office is already processing applications.

This is a screenshot from Moran’s campaign Facebook page. The red line was added.

The problem is that, according to both the available documents and his remarks at the October 31 pre-agenda meeting, it was not up on Friday.

In this clip from the Friday meeting, he tells his colleagues that it would take twenty-four hours for the vendor to deploy it. He then says, presumably because the next day is the weekend, it would not be up until Tuesday.

So if it takes twenty-four hours and if he advised his colleagues of this on Friday morning, it could not possibly have been available that night.

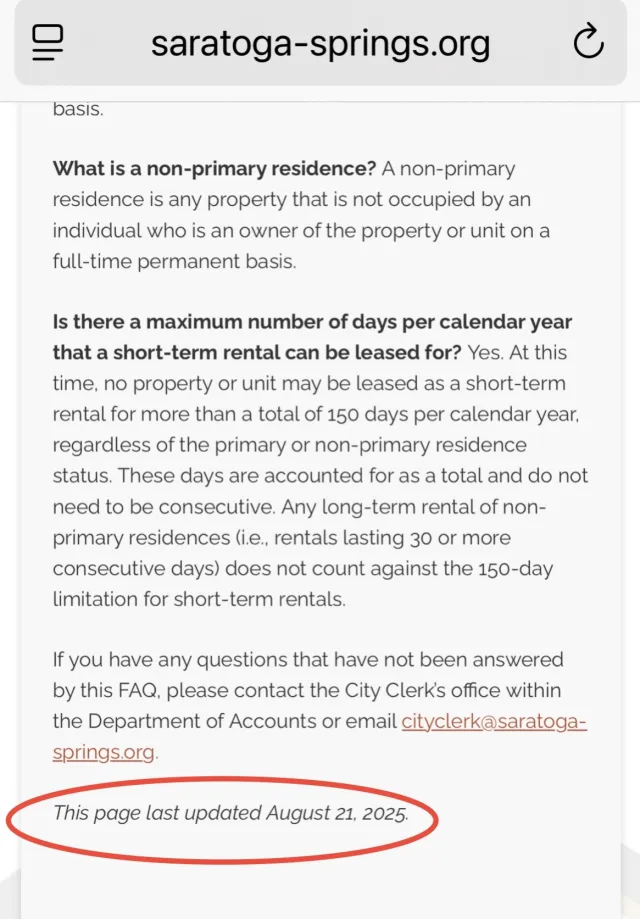

In addition, this time stamped city website page from Saturday morning, November 1, shows that the page had not been updated since August,

Dillon Moran’s Short Term Rental Fiasco

Saratoga Springs Accounts Commissioner Dillon Moran has promoted himself as the successful architect of short-term rental management. In fact, his campaign mailing focuses on this as one of his main achievements.

A casual scrutiny of what he has actually done and not done reveals a very different story.

Moran had the city purchase the software for a portal to be used by short-term rental owners to register with the city. It was purchased on February 6, 2024. The cost for using the software for the first year was $56,000.00. It was not deployed, so the city wasted the money for that year. On February 6, 2025, the city paid for the next year in the amount of $55,000.00. By his own admission, the portal will not be functional until the end of the year, so that is another $55,000.00 wasted.

During this period, he successfully received support from the city’s civil service to hire an additional staff member to handle STRs. As the software has not been deployed, hiring anyone was premature. He also successfully raised the salaries of employees in his office because the alleged workload for STR was added to their responsibilities.

Accounts employee X was hired on July 26, 2023, at a salary of $66,668.00. On February 20,2024, her salary was increased to $83,380.00 to compensate her for her additional duties with STR. The new budget crafted by Minita Sanghvi raises her salary to $92,687.00

Moran has routinely announced at City Council meetings one date after another that the STR software would be deployed. In fact, on October 20, 2025, at the League of Women Voters forum, he announced it would be up the next day. Of course it was not. The latest date he has announced is now December 31, 2025.

There is further confusion because the annual registration date, which involves a fee, is in June. Therefore, if the owner of an STR registers on January 1, 2026, (it remains to be seen if the portal will be operational), they will be required to register at the full rate for a year, with their registration expiring in June.

There is also the problem that these STRs must be inspected by the city, and it remains to be seen when this will happen and how long it will take.

Many of the folks with short-term rentals are, not surprisingly, frustrated and angry at the mess that Moran has created.

This is yet another example of Moran’s desire for headlines and his utter failure to actually manage.

Saratoga Democrats Close Their Campaign with a Big Beautiful Lie; Will It Work In This Election?

The Saratoga Springs Democratic Party has sent out their final campaign mailer. Interestingly, it doesn’t tout their platform or even mention who their candidates are. No, the message the local Dems want to leave their audience with is its phony claim that One Saratoga is a tool of the MAGA GOP. This is the local Dems oft repeated big beautiful lie that they hope will win them this election. The Dems do not seem to realize that this kind of over-the-top attack only serves to damage their local committee’s reputation and their endorsed candidates. If they would lie so blatantly in this kind of mailing, how can people trust what their candidates will say if they are elected/re-elected?

The best antidote to this kind of campaigning is to share with the public who One Saratoga is. So here are two members of One Saratoga who the local Dems want you to believe are really MAGA operatives. You decide.

Courtney DeLeonardis, Chair of One Saratoga, Addresses The Voters

Jane Weihe, Campaign Assistant, One Saratoga Addresses The Voters

Lew Benton Dissects Minita Sanghvi’s 2024 City Budget To Describe The Roots Of Today’s Financial Crisis

[I received this essay from Lew Benton. This year was not the first time Sanghvi has mishandled the budget process. Lew goes back to 2023 to detail how Sanghvi failed to follow best practices and charter requirements in putting together the 2024 budget. He notes also her penchant for consistently overestimating revenues and underestimating expenditures which has contributed to today’s dilemma. ]

Why Make the Proposed City Budget Opaque?

Perhaps some of those who attempted to review the City’s October 27 amended Comprehensive Budget, and compare and contrast it to the Finance Commissioner’s initial October 3 presentation, came away as perplexed as Alan Turing in his early efforts to crack the Enigma Code.

If you did, you were not alone. Unlike all previous City budgets, the proposed amended 2024 budget does not adhere to the format required by the City Charter.

Rather than, as outlined in the Charter, follow a standardized budget format that employs “ … the most feasible combination of expenditure classifications by funds, organization unit, program, purpose, or activity and object,” all proposed expenditure lines are lumped together, not disaggregated by function.

The table below presents the City Attorney’s Budget as it appeared in the proposed 2024 Comprehensive spending plan dated October 3, 2023. The expenditure budget for each of the departments under the mayor’s administrative control follows the same format, as does each organizational unit or function in Finance, Accounts, Public Safety and Public Works.

CITY ATTORNEY’S OFFICE

PERSONAL SERVICE 2022 2023 2023 2023 2023 2024

Original Adopted Revised Actual Projected Comprehensive

A301142151047 FOIL OFFIC .00 .00 .00 .00 .00 .00

A301142151090 CITY ATTY 89,493 93,600 93,600 71,742 93,857 93,857

A301142151110 ASST ATTY .00 .00 82,548 57,743 82,549 105,276

A301142151117 AST CITY A .00 .00 .00 .00 .00 .00

A301142151276 EXASSISTAN 53,496 54,566 57,297 43,796 57,297 59,550

A301142158030 SS CITY PO 10,913 16,689 23,004 13,059 17,878 19,789

TOTAL PERSONAL SER VICES 153,902 164,855 256,449 186,342 251,581 278,473

EQUIPMENT AND CAPITAL OUTLAY

A301142252200 OFFICE EQ 1,360. 00 .00 .00 .00 .00

TOTAL EQUIPMENT AND CAPITAL 1,360. 00 .00 .00 .00 .00

CONTRACTED SERVICES

A301142454110 OFFICE SUP 3,019 700 700 559 700 700

A301142454120 POSTAGE 346 350 355 355 355 350

A301142454250 CONF REG 509 1,500 870 107 870 .00

A301142454440 BOOKS 1,195 1,300 2,044 943 1,687 1,300

A301142454671 PHONE FAX 31 .00 216 170 216 .00

A301142454720 PROF SER 92,816 20,000 56,250 33,049 92,312 20,000

A301142454740 SC EQUIP 2,163 2,050 2,050 1,335 2,050 2,050

A301142454745 LEGAL LIAB .00 .00 .00 .00 .00 .00

A301142454760 LEGAL 500 750 750 500 750 750

TOTAL CONTRACTED SERVICES 100,581 26,650 63,236 37,020 98,941 25,150

TOTAL CITY ATTORNEY 255,844 191,505 319,686 223,363 350,523 303,623

This format allows ease of access and review of the proposed budgets of each city function, identification of and individual expenditure for each title, non-personal costs and costs of associated contractual expenses. Further, this format – required by Charter law – shows the total costs for each expenditure classification.

In this example, it is noted that the Council has significantly overspent the “PROF SER” line this fiscal year and last. This should beg the question of why over $90,000 has been spent in 2022 and 2023 on outside legal services while only $20,000 was initially budgeted. And why only $20,000 is proposed for 2024.

Is this an anomaly? Were there unanticipated extra-legal services in 2022 and 2023 that will not be necessary in 2024? Of course many other similar observations are made in the review of essentially all departmental budgets.

This required budget presentation is transparent, relatively simple and allows and encourages understanding. The amended budget is opaque.

Without explanation, however, the proposed amended 2024 Comprehensive Budget is presented in an entirely different form.

For example, the several “department” expenditure lines under the auspices of the mayor are simply thrown together, co-mingled. The reviewer is left to divine which line items are part of which of the mayor’s several department budgets: i.e., City Attorney, Planning, Building, Human Resources, etc.

The same is true for Finance, Accounts, Public Safety and Public Works. In the later two, Public Safety and Public Works, the task of meaningful, comprehensive review of the budgets of discrete functions: i.e., fire services, policing, EMS, etc., requires substantial investment in time and enough working knowledge to assign each line item to its respective agency.

In the Mayor’s proposed budget there are at least seven expenditure lines alone labeled “Professional Services” but the only way to determine which department the lines apply to requires a time consuming and tedious matching of account numbers.

Why Finance elected to abandon a budget format that has always been relatively easy to read and understand for one significantly more difficult to puzzle out is itself a conundrum. Finance must be required to reformat the proposed amended budget before its November 28 hearing.

Other Thoughts on the Proposed 2024 City Budget. Certain Revenues

and Expenditures

The proposed 2024 City Comprehensive Budget as presently constructed is concerning. It will require significant amendments if operating deficits are to be avoided next year.

First and foremost, it includes unfavorable budget variances in both major revenue and expenditure accounts.

This comes on the heels of a 2023 budget, the first prepared and adopted by current City Council members, that preordained the 2024 proposal’s many overstated anticipated revenues and, in some cases, grossly underfunded expenditure lines.

The proposed 2024 operating budget is not in balance and must not be adopted until it is. To bring it into balance will require a more realistic examination of several accounts, including those referenced below, and the political will to act.

No doubt, the lack of institutional knowledge and limited understanding of how this government functions on the part of a Council made of first term members can, in part, serve to temper the inadequacies in the 2023 budget. But failure to recognize and correct them going forward is unacceptable and a violation of the fiduciary’s responsibility.

Attempting to transfer blame to those who had no hand in the adoption of the 2023 budget or the preparation of the 2024 plan, citing recent high inflation and the dearth of new revenue streams for the city’s fiscal difficulties rings hollow.

All local governments are faced with the same head winds. It might be more honest to acknowledge that hiring additional non-essential employees was not prudent, that budgeting non-existent revenues e and that deliberately low balling major expenditures invites deficit spending.

Following are examples of the unfavorable variances in the proposed 2024 operating budget. There are, to be sure, others.

Revenues

In Finance, $850,000 in Hotel Occupancy Tax revenue is proposed for 2024. This is over $100,000 more than was actually realized in FY 2022 and over $600,000 more than has been received to date this year.

The 2023 budget includes a non-existent ‘Cannabis Tax’ revenue of $250,000. The proposed 2024 budget carries that same amount forward. Potential first time revenues such as this one do not usually meet expectations. And by prematurely including the revenue in the 2023 budget only added to a negative revenue variance

The proposed Mortgage Tax revenue for 2024 is $1.5 million compared to the $933,400 collected to date this year. The $933,400 is far below the $2.05 million budget.

Mortgage markets have been depressed even here in Saratoga Springs by Fed attempts to reign in inflation. Even the $1.5 million proposed seems unrealistic.

The Mayor’s budget is ripe with unfavorable 2024 revenue variances. The Building Permit account carries a proposed $700,000 revenue even in the face of a major decline in permit revenues this year. To date Building Permit revenue is listed by Finance at $352,520 with only $400,000 projected by the end of the FY. This is $300,000 less than was budgeted. Artificially inflating anticipated revenue only increases the structural deficit.

In recent years this revenue has been strong but, at least for the short term, it is most unlikely that in one year that revenue will increase 75%, from $400,000 to $700,000.

Likewise, Planning Board fees are unrealistically overstated. Actual 2022 Planning Board revenue was $122,820. Still, this revenue line was increased to $200,000 in the adopted 2023 budget but is now projected by Finance to fall $35,000 short.

Now, in spite of the anticipated 2023 unfavorable variance, Finance has increased the line to $250,000 for 2024. Perhaps an explanation for this doubling of the 2022 revenue and increasing the anticipated 2023 collections by $85,000 in the 2024 budget is in order.

Other revenue lines in the Mayor’s budget that are suspect include Insurance Reimbursement, from -0- this year to $125,000 next year.

The Public Safety revenue budget includes a $300,000 increase in Ambulance Transportation charges over the $2 million projected to be realized by the end of FY-23 and is over $500,000 more than actually collected in 2022.

Unless the fee structure has been significantly increased this revenue line is likely to fall far short of the $2.3 million in the proposed 2024 budget.

Parking Enforcement revenue is now anticipate to be $462,0000 this year, down almost $80,000 from the $540,000 budgeted and $38,000 less than the $500,000 in the 2024 proposal.

Operating Expenditures

The operating budget also includes many likely unfavorable variances. Just as overestimating revenues in the actual 2003 and proposed 2024 budgets contributed to the city’s present fiscal dilemma, so have what appears to be unfavorable variances in the operating budgets.

In the 2023 Public Safety operating budget the City Council included $190,000 for Fire Fighter Overtime. Finance now projects that by the end of the fiscal year $533,500 will be spent, this is an astronomical increase of $343,500 over the amount budgeted.

Similarly the Firefighter Compensation Time budget is anticipated to be overspent. Only $190,000 was earmarked for this line in the 2023 budget but $563,000 is anticipated to be spent by year’s end, a $373.000 overage.

So too is the proposed 2024 Police Overtime and Compensation Time lines grossly underfunded. Finance proposes to appropriate the rather odd amount of $263,637 for Compensation Time vis a’vis the $483,570 spent in 2022 and the projected $450,000 in 2023. The 2024 OT line is set at $325,000 against the $507,505 expended in 2022 and the estimated $450,000 this year.

In the aggregate, Finance is proposing 2024 Police and Fire Fighter OT and Comp Time expenditures totaling $1,338,637 although corresponding 2022 costs were $1,498,271 and projected 2023 expenditures are $1,981,000.

While there may have been unique circumstances that have resulted in higher than normal Police and Firefighter OT and Compensation Time expenditures this year, the proposed 2024 appropriations are well below what will be needed to avoid the necessity of transferring large amounts during the course of FY 24.

In the Mayor’s office $20,000 was budgeted for outside legal counsel this year but Finance projects that over $92,000 will be spent. Only $20,000 is earmarked for next year. Now it appears that yet more outside legal services will be retained to investigate an offending mail. This is madness.

These references are not all inclusive. There are many more questions to be asked and answered. Why, for example has Code Blue shelter support been cut from the budget.

There is time to prepare a more realistic 2024 operating budget. I hope the City Council will do so lest the new Council be bequeathed an extraordinary fiscal challenge.

Lew Benton